Paramount Corporation Bhd has long been known for being involved in both the property and education sectors. However, Group CEO Jeffrey Chew believes its future will most likely lie in it becoming a pure real estate company.

Currently, the group’s profits comprise contributions from property (about 69%) and education (31%).

However, with its education segment providing mixed results, Paramount is looking at ways to monetise its educational sector assets. This could result in the company completely exiting the sector.

According to Chew, the group is mulling ‘strategic divestments’ which could see it offloading stakes in its education assets to strategic partners.

“We cannot commit to whether we will exit to a certain percentage or totally as it depends on the proposition we receive. (But) we are open either way so long as it can move the franchise forward,” says Chew.

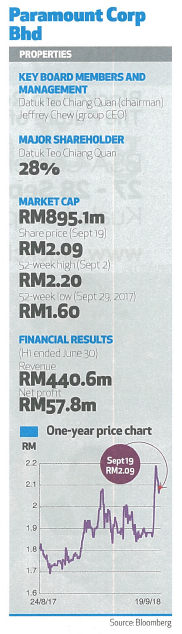

According to an RHB Research report by Loong Kok Wen, the move to monetise its education assets makes sense for Paramount and should prove to be an important boost to its share price.

“The value-unlocking effort for the education division is still ongoing, and this remains the key share price catalyst for the stock over the medium term,” she opines.

If Paramount does totally exit the education space over the next few years, Chew is confident that the property business will be able to make up for the loss of revenue.

“We love the education segment because it provides consistency, has less volatility and is a very positive cash flow type of business,” he notes.

“But on the other hand I think we are very much a property company and see ourselves as very much a pure play property company going into the future.”

During Chew’s tenure which began in July 2014, the group has grown its sales from RM300 mil in 2014 to RM1 bil in 2017.

This has contributed to its revenue rising to RM763 mil from RM510 mil, boosting profit before tax to RM183 mil from RM86 mil over the same period.

“We will continue to grow sales from the RM1 bil level over the next five years to maybe RM1.5 bil, although it will not be that aggressive anymore because we feel that we have reached a stage where we are of adequate size.

“So growing in the teens (in terms of percentage) per year over the next five years and hopefully we can maintain the profit margin of around 15% which we have been enjoying.

“This will give a good size of profits from our property development,” explains Chew.

Growing Sales

Chew has taken several steps to improve Paramount’s sales that in turn are leading to better profits. One key move was to increase the number of projects being under-taken at any one period.

Paramount used to rely on the revenue contributions from just two or three projects.

But this has changed to about eight projects at a time, and this makes the contribution to turnover “well diversified and a little bit more sustained.”

“It is not like you have two projects and one goes off and your turnover drops in half. We now have a lot more predictability and sustainability in terms of revenue being generated from our property segment,” he adds.

The group is also fully aware that to sell houses in the current environment it has to make sure its properties are suitably priced and cater to what buyers need.

“In past years, we focused on properties in the RM500,000 to RM800,000 bracket. But after a lot of research into the statistics and the different data available, we realised that most can only afford products of about RM300,000 to RM400,000 – the sweet spot.

“So, over the past two years we have actually switched our products to make them a little bit more affordable (although these are not affordable housing projects) like a RM400,000 type property, by making them a little bit smaller but very functional.

“We trim the luxury features that we used to have and try to make sure the price is suitable for the market, especially in the Klang Valley,” explains Chew.

So while the group still has its higher end projects, most of its projects are priced at the mid-tier level.

He believes that this is one of the reasons Paramount’s sales has been able to keep on growing despite the softer market.

Key Contributors To New Sales

In the first half of financial year 2018 (H1FY18), new sales amounted to RM598 mil, which includes the Kota Damansara land sale.

Key contributors were its Atwater project in Petaling Jaya and Suasana Phase 1 at Utropolis Batu Kawan, notes RHB Research’s Loong.

She expects Paramount to hit its RM1 bil sales target for the financial year under review.

“Since its launch in Q1FY18, Atwater has achieved a take-up rate of about 6o%, which is commendable in a slow property market.

“Meanwhile, the newly launched Keranji@Greenwoods Salak Perdana also contributed. We expect more bookings to be converted to sales from these two projects in Q3,” she adds.

RH Research has a buy rating on the counter.

Paramount is also looking to establish itself in the wider real estate industry by venturing into the land development business.

Chew says that in the event Paramount can get a better or equal return on land it owns by selling it to another party, it will do so.

Its recent disposal of 3.8ha of industrial land in Kota Damansara to EM Hub Sdn Bhd for RM92.1 mil is an example this.

Chew explains that the group has found that selling the land to a third party could offer it similar or even better returns than developing it by itself.

He is hopeful that this new venture will increase profits by 20% to 30%. This will also help plug the gap arising from the loss of profits from the education side should the group undertake strategic divestment in this area.

Meanwhile, projects such as Paramount’s co-working spaces will help provide recurring income for the group. To date, the group has launched two such projects including a 20,000sq ft space that was opened in Starling Mall, Petaling.Jaya, in July 2018.

It also hopes to get steady rental rates from its Utropolis mall in Shah Alam.

“This will narrow the gap to an extent, if we do divest (from its education business),” he says.

—

—

Paramount’s tale of two sides of its education play

Education

A complete exit from the education game may not happen soon. Hence, in the meantime Paramount needs to find ways to generate returns from its education business given how much it has invested in the area.So far, the education business has been a tale of two halves.

The K-12 portion equivalent to kindergarten, primary and secondary of its education portfolio has been making money.

Its Sri KDU school has been performing very well and it is now building its second private school in Klang.

It had acquired the REAL Education Group last year, which helped make it the largest private K-12 school operator in Malaysia.

“This has made us very well established and we’ve got a lot of parties from overseas looking at how they can work with us through strategic partnerships or wanting to make an investment in our company,” Chew notes.

Given the strength of the K-12 segment, Paramount was able to monetise its assets, having sold its Sri KDU campus in October 2017.

Despite having to now pay rental to use utilise the school and its facilities, its operating margins and profits are enough to cover the cost of rental.

In contrast, its tertiary segment has struggled amidst a competitive and saturated market and is now recording losses.

“The tertiary market has been so saturated that every seven and a half students out of 10 who graduate SPM will have a university place whether in private or public university,” he details.

While good for the nation as this will result in a highly educated workforce, it poses a challenge to university operators.

This is because university operators are unable to raise fees even though other costs continue to rise, while still having to invest in their campuses and facilities in order to attract students.

In an effort to stem its losses, Paramount has been trying to revamp and reposition its tertiary business.

Its key initiative has been to position itself as an expert in three main education areas – hospitality and culinary arts, computing and creative media, and entrepreneurship.

“By doing that we have been able to increase our enrolment by more than 10% over the past four years, but the thing is, when you have a campus built for 7,000 students and you started off with fewer than 2,000, it will take time,” he explains.

Paramount has invested RM260 mil and will invest another RM130 mil to build a campus in Batu Kawan. In total, its tertiary assets are about RM500 mil. The group ultimately would like to monetise these assets but Chew says that is difficult to do so given the fact that it is incurring losses at the moment. “To monetise the assets, you must be able to pay the rental,” he points out. “So, we have RM500 mil worth of assets which we are unable to crystallise into any real valuation until we make decent profits.” Despite the challenges, Chew believes that the tertiary segment has made good headway over the past four years.

Lifting The Game

He opines that the group needs to take a few more steps to further lift the brand. It is trying to achieve this through its own initiatives and through strategic partnerships.“This is so we can create better programmes, charge higher fees and also attract international students,” he says.

“We want to lift the game, which means offering better quality qualifications and more importantly, the ability to get a good job in the marketplace.”

With its K-12 segment generating profits and its tertiary arm not, it can perhaps be seen to be counterintuitive for Paramount to be open to divesting in both segments. However, Chew points out that it is difficult to offload something that is not making money.

“When you try to sell something that is not doing well, you will not get any money for it. It is when you are doing well that you want to exit.

“Paramount’s K-12 business and the REAL Education Group have made it a very attractive education platform in Malaysia. From this it can even expand into oilier countries and people see value in this business.

“Our K-12 assets have a market valuation of around RM600 to RM700 mil. If somebody wants to buy it or have a strategic stake in it, we do not see why we should be averse to it,” he argues.

Given that its tertiary education division is still making losses it will be difficult to get a strong valuation for it.

Therefore, Paramount will have to improve this segment before it can start to look at divestment options, he adds.

Future Plans

In the meantime, in line with its plans to move towards being a pure-play property player, Paramount is looking at venturing overseas.Chew says that over the past five years the goal has been to consolidate local operations and build scale.

“Now that we have reached the RM1 bil and beyond level, we may be in a position over the next five years to venture into projects beyond Malaysia,” he suggests.

There are no projects underway or any particular locations in focus, although it does have a piece of land in Australia following a joint venture with an Australian company which it entered into in June 2011.

“Nothing is happening yet, but we think that opportunities will start to come,” he says.

—

Addressing the housing mismatch

Paramount Corporation Berhad’s Group CEO Jeffrey Chew disagrees with the commonly held belief that there is a housing oversupply in Malaysia.Rather, he believes there is a mismatch between what is being supplied and what the consumer wants.

“We always talk about supply and if there is an overhang but I think we have to look at both the supply and the demand,’ he says.

Malaysia has a population of 32 million people and the population growth is about 1%, with a demographic that remains young. Census estimates say the number of new households in Malaysia is still growing at about 2.9% yearly.

“If you have about 7.4 million households in Malaysia then you get about 200,000 plus in new demand for houses per year,’ suggests Chew.

“We do not have that kind of supply. If you look at the National Property Information Centre (NAPIC) report you will see that across Malaysia you only have about 606,000 houses under construction. This takes about three and half years to complete, so we release into the market an estimated 160,000 or so houses annually.’ he points out.

“If you compare the number of houses being built per year and the estimated rise in demand for homes, then every year you have a potential shortfall of around 40,000 households that will likely need a home sooner or later.’ he adds.

Therefore, the main reason for unsold units is because there is a mismatch in factors such as location and affordability, among others.

Chew believes that dealing with this is the biggest challenge for all parties, particularly the government and developers.

“It is a question of how you get proper data so that we can build houses at the right location and affordability levels, which is a product that people want,’ Chew argues.

Cost Of Building

He says the other factor that needs to be addressed is the cost of building houses, which has been rising very sharply over the past five years.“Land, construction, labour costs have all been going up. Then you have contribution and compliance costs that also have escalated in line with the valuation of the land,’ he points out. “This has made it challenging for developers to build houses cheaply’.

While consumers want cheap homes, developers have to consider many factors, particularly securing funding and giving their shareholders value.

“Most developers obtain funding from the bank; if our margins are very low, the bank will reject the loan. So, we need to make sure our projects are a mix of affordable homes- where the margins are low- and market-driven products where the margins are reasonable so we can get the loans.

“Then after all this we must deliver some returns to our shareholders as they are our primary responsibility as a listed company.

“Or else they will sell your shares because they are not getting any returns on their investments,” notes Chew.

Therefore, he argues, it is unfair to expect the developer to take full responsibility to provide affordable or social housing.

Partnering The Government

Chew opines that the best way forward is for all parties to work more closely to deal with this problem.“Whether is with the government, the banks or the state authorities, we need to work together to take care of the social housing needs,’ he says.

He does not think it is possible to just lower the current prices of houses significantly because this will affect the current value of homes and cause wealth destruction for those who own them.

Instead, Chew says, there must be an effort to slow the escalating house prices by managing the costs that go into building them.

One way is to cap the compliance costs that are levied on developers, suggest Chew. Another is to control the land prices for developers of affordable homes.

The government, developers and other parties should take these factors into consideration, in order to contain the rising housing prices for the next five, 10 or even 20 years, he argues.

This will hopefully enable people to buy homes suited to their affordability.